Splitting a purchase into four easy payments sounds like a smart move: no interest, no credit card, no problem. At least, that is what the checkout screen suggests. Millions of people tap “Pay in 4” every single day without giving it a second thought.

But Buy Now, Pay Later is more complicated than the name implies. The cost structure is different from a credit card; the risks are less obvious, and the fine print is easy to miss when you are already excited about what you are buying. This article pulls back the curtain on Buy Now, Pay Later, explains how it really works, and shows you exactly what it can cost when things do not go according to plan.

The problem is not a lack of discipline. The problem is that most budget systems are built on assumptions that don’t reflect how real people live, spend, and think about money. Understanding why budgets fail is the first step toward building a personal budget that actually works. This article breaks down the real reasons traditional systems collapse. It introduces a simpler approach that focuses on three numbers instead of dozens of categories.

Watch the Money Nudge YouTube Video about the definition of Finance:

Prefer to watch instead of read?

Subscribe to The Money Nudge on YouTube for plain-English videos on money, investing, and economic topics.

Table of Contents

What Is Buy Now, Pay Later?

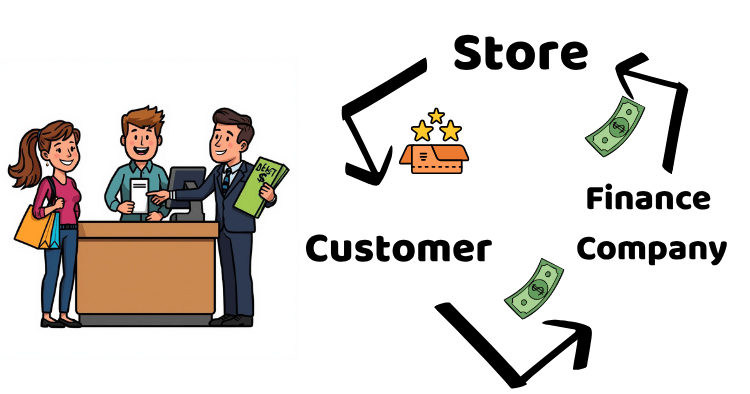

Buy Now, Pay Later (BNPL) works like a short-term loan attached to your shopping cart. A financing company steps in at checkout, covers your full purchase price immediately, and you repay that company in equal installments over the following weeks or months. You leave the store with your item, and your obligation shifts entirely to the financing provider.

Four equal installments are the most widely used BNPL format. The first is collected at the time of purchase, and the remaining three are collected at two-week intervals. On a $200 purchase, that works out to $50 at checkout, then $50 on each of the three dates that follow over the next six weeks.

Dedicated BNPL providers operate across most major retail categories, and many large retailers have built their own installment tools directly into the checkout process. Technology companies and major payment platforms have also introduced their own versions, which now appear routinely at the end of online orders.

The appeal is straightforward. You get what you want today and spread the financial impact across multiple paychecks. For someone short on funds today but expecting money soon, it feels like a practical bridge.

How Does BNPL Actually Work?

The mechanics are simple at the surface, but the details vary by provider and by the size of the purchase.

Selecting BNPL at checkout triggers a behind-the-scenes transaction. The financing company pays the retailer the full purchase price right away. Your debt now belongs to that financing company, not the store. The store is done. Everything from that point forward is between you and the BNPL provider.

For smaller purchases, the Pay in 4 model handles things automatically. Payments are charged to your linked debit card or bank account on a fixed schedule. The money leaves your account on the scheduled date, regardless of whether you actively track it.

For larger purchases, some providers offer extended repayment windows of 3, 6, 12 months, or longer. These plans often carry interest, which changes the math considerably. A plan marketed as “0% financing for 6 months” is not always interest-free. Some providers apply deferred interest charges, meaning the lender calculates interest retroactively from the original purchase date if a balance remains when the promotional window closes.

Read that carefully. Deferred interest is not the same as zero interest. It is a retroactive penalty applied to the full original purchase amount, even when you made every scheduled payment along the way.

Why BNPL Feels Different From a Credit Card

One of the biggest reasons BNPL has grown so quickly is that it does not feel like debt. That perception directly shapes how people spend when using it.

A credit card delivers one bill at the end of the month. All charges appear together. The total owed is visible in one place. BNPL breaks the same cost into smaller, more manageable pieces. That fragmentation makes spending feel lighter than the math actually supports.

Behavioral researchers call this the “pain of paying.” Large, immediate payments trigger a psychological resistance that naturally slows spending. Smaller installments reduce that resistance significantly. BNPL platforms are designed specifically to lower that barrier, which is why they are so effective at driving purchases that might not have happened otherwise.

Speed is another factor. Applying for a credit card takes time and often involves a credit check. BNPL approvals happen in seconds, often with only a soft check that leaves no mark on your credit report. No credit card is required. For younger shoppers without an established credit history, BNPL fills a gap that traditional credit products cannot.

None of that is automatically harmful. Understanding the psychology at play, however, puts you in a better position before you reach for the installment option at checkout.

The Real Cost of Buy Now, Pay Later

Here is where things get specific. BNPL is not free, even when it appears to be. The costs appear differently depending on the provider, plan length, and your payment history.

Late Fees

Missing a BNPL payment triggers a late fee. Amounts vary by provider, but charges typically range from $5 to $15 per missed payment. Some providers add a second fee if the account stays delinquent beyond a certain number of days. One major provider, for example, applies a $10 late fee on qualifying orders. If that missed payment remains unresolved for another 7 days, an additional $7 is added. A single slip on a $200 order turns a supposedly free service into a $17 lesson.

Interest on Longer Plans

Longer BNPL plans frequently carry interest, and the annual percentage rate can be substantial. Rates vary by provider, your credit profile, and the plan you select. Depending on those factors, APR can range from 0% to 36%. At 30% APR on a $1,000 purchase repaid over 12 months, you would pay $167 in interest, bringing your actual total to $1,167 rather than $1,000.

Hold that against a credit card charging 20% APR, and the BNPL plan at 30% becomes the more expensive option. The installment format disguises the cost, but the underlying math remains the same.

What if I tell you that the Interest Rate is not the same as the APR?

Read Article →Deferred Interest Traps

Some BNPL plans advertise 0% financing for a set promotional period. If you carry any remaining balance past that deadline, the lender applies deferred interest retroactively to the full original purchase amount. This is one of the most financially damaging features in the BNPL space because it catches people off guard.

Consider this: you finance a $1,500 laptop under a 12-month 0% promotional plan. You make every payment on time, but still have $200 remaining at month 12. When month 13 arrives, the lender calculates deferred interest at 29.99% against the original $1,500 balance, not just the $200 you still owe. That single retroactive charge could exceed $450, added to the remaining balance all at once.

Before accepting any plan that advertises a promotional period, read the full terms. One overlooked clause can transform months of disciplined payments into an unexpected penalty.

Overdraft and NSF Fees From Your Bank

BNPL withdrawals happen automatically on scheduled dates. When your account balance falls short on that day, your bank may charge an overdraft or non-sufficient funds fee, typically somewhere between $25 and $35. That charge comes from your bank and is entirely separate from any late fee the BNPL provider may also apply. A single missed BNPL payment can trigger fees from two companies at once, pushing the combined cost to $40 or $50 in a matter of hours.

How BNPL Affects Your Credit Score

This is one of the most misunderstood parts of Buy Now, Pay Later. The impact on your credit depends heavily on which provider you use and what type of plan you select.

The Soft vs. Hard Credit Check Divide

Short-term installment plans typically run a soft inquiry during the approval process. A soft inquiry produces no record on your credit report and does not affect your score in either direction. That accessibility is a core reason BNPL attracts shoppers who are still building their financial history. Extended financing plans, however, often require a full credit review, which counts as a hard inquiry and can temporarily reduce your score by a small amount.

Reporting to Credit Bureaus

BNPL providers differ widely on whether they share payment activity with the three major credit bureaus: Equifax, Experian, and TransUnion. Many providers report nothing, so every on-time payment you make builds no credit history. Others do report, which means a missed payment can damage your score directly.

Both Equifax and Experian have moved to incorporate BNPL activity into their systems in recent years. Experian introduced a dedicated BNPL credit file to track this data separately from traditional accounts. As more providers begin reporting activity across all three bureaus, the consequences of missed payments will likely grow.

The pattern holds across providers: responsible BNPL use rarely builds your credit, but a missed payment can damage it.

Debt-to-Income Ratio

Even when BNPL balances go unreported to the credit bureaus, lenders increasingly look for active BNPL accounts when reviewing mortgage and loan applications. A stack of ongoing BNPL obligations signals that you are carrying more financial commitment than your bank statement reflects. That can work against you during the underwriting process, even when your credit score looks fine.

The BNPL Debt Spiral: What It Looks Like in Real Life

Here is a pattern that plays out more frequently than most people expect.

Someone uses BNPL to buy a jacket. Two weeks later, the same service covers a birthday gift. A month after that, a six-month plan finances new kitchen appliances. Within three months, four active BNPL plans are running simultaneously, each pulling automated payments from the same bank account on different dates throughout the month.

None of those purchases seemed unreasonable on their own. But four overlapping payment schedules can add up to something that rivals a monthly car payment. Credit cards consolidate all charges into a single monthly statement. BNPL does not. The total financial weight stays scattered across separate apps until the pressure becomes hard to ignore.

Research from the Consumer Financial Protection Bureau identified a consistent pattern among people who rely heavily on BNPL. Frequent BNPL users showed higher rates of carrying revolving credit card balances, borrowing from payday lenders, and experiencing overdrafts than people who do not use installment services. BNPL did not necessarily create those conditions, but the correlation with broader financial stress was clear.

Who BNPL Is Designed For — and Who Uses It

BNPL companies build their products around a specific type of customer: someone who wants immediate access to a purchase, prefers breaking costs into smaller payments, and either lacks access to traditional credit or prefers to avoid it entirely. Onboarding is fast, approval feels easy, and the checkout experience is built to keep friction low.

In practice, younger consumers use BNPL more often. Gen Z and Millennial shoppers represent the largest share of active users. A notable portion of that group consists of lower-income individuals using installment plans not for luxury purchases but for everyday essentials, including groceries, clothing, and household basics.

That reality is a meaningful departure from how these products were originally framed. When BNPL services launched, the pitch was about giving shoppers flexibility on larger, occasional purchases. Today, many people use installment plans to cover expenses they cannot fully absorb at once, splitting a $60 grocery run into four $15 payments to get through the week.

A tool used that way is not solving a cash flow problem. It is deferring one while making the next one more likely.

BNPL vs. Credit Cards: A Fair Comparison

Buy Now, Pay Later and credit cards serve some overlapping purposes, but the two products work quite differently. Understanding where they diverge helps you choose the right option for a given situation.

| Factor | Buy now, pay later (BNPL) | Credit Card |

|---|---|---|

| Approval Speed: | Seconds | Days to weeks |

| Interest (Short-term): | Often 0% for Pay in 4 installments | 0% only with promotional offer |

| Interest (Long-Term): | 0% to 36% APR | 15% to 29% APR Typical |

| Late fees: | $5 to $15 per incident | $25 to $40 per incident |

| Credit building: | Rate, inconsistent | Yes, with responsible use |

| Rewards: | None | Points, cashback, miles |

| Spending visibility: | Fragmented across apps | Consolidated monthly statement |

| Consumer Protections: | Limited | Strong (dispute rights, fraud coverage) |

When managed well and paid in full each month, a credit card delivers something BNPL cannot: a payment history that builds credit, rewards that add genuine value, and legal consumer protections that give you a real path when a purchase goes wrong. BNPL, on the other hand, is faster to access, requires no prior credit relationship, and suits people who either do not have a card or prefer to keep credit card balances at zero.

Neither product is universally better. The key is understanding what each one actually costs before you commit.

When BNPL Can Make Sense

Not every use of Buy Now, Pay Later is a financial mistake. There are situations where it functions as a reasonable, low-cost tool.

A genuine short-term cash flow gap. If a work-related purchase is needed before your next paycheck arrives, and you know with confidence that the money is coming, a 0% Pay in 4 plan costs less than putting the charge on a credit card and carrying a balance into the next billing cycle.

A 0% promotional plan with a clear payoff date. If the plan carries no deferred interest and you set a specific repayment schedule you can track, a longer BNPL plan can serve as an interest-free bridge for a purchase you already planned to make.

A single plan, not several running at once. One active BNPL balance is manageable. Running four or five in parallel is where the math starts working against you.

The difference between a useful tool and a financial trap often comes down to one question: Did you plan this purchase before the BNPL option appeared, or did the installment option make a purchase feel affordable that you could not otherwise cover?

Practical Steps to Use BNPL Safely

If you choose to use BNPL, a few habits can protect you from the most common problems.

Track every active plan in one place. Keep a running note or spreadsheet listing each plan, the payment amount, and the withdrawal date. BNPL apps are fragmented. Each provider runs its own separate platform, and none of them communicate with each other. You are the only person with the full picture.

Check your bank balance before each payment date. Set a calendar reminder a day or two ahead of each scheduled withdrawal. Do not assume the funds will be there simply because you expect them.

Limit yourself to one active plan at a time. This is the most effective single habit for keeping BNPL manageable. One plan is trackable. Multiple overlapping plans create a payment schedule that is easy to lose track of and difficult to recover from once payments start being missed.

Keep BNPL away from recurring expenses. Using installment plans for groceries, utilities, or subscriptions builds a cycle that is difficult to exit. Spreading regular, recurring costs across future paychecks means those future paychecks arrive already partially committed.

Read the complete terms before confirming any plan. Scan specifically for the phrase “deferred interest.” If you find it, understand precisely what happens to your balance if any amount remains after the promotional period ends.

The Bigger Picture: BNPL and Your Financial Health

Buy Now, Pay Later is not inherently good or bad. It is a financial product, and like most financial products, the outcome depends almost entirely on how it is used.

The companies behind BNPL are not charities. Revenue comes from late fees, from interest on extended plans, and from merchant fees that retailers pay in exchange for the conversion lift that installment options provide. These platforms are designed to be easy to say yes to. That ease is the product.

Understanding the business model does not mean avoiding BNPL entirely. It means approaching each checkout decision with a clearer picture than the payment screen provides. The screen will always make it look simple. Your job is to run the actual numbers before tapping confirm.

A $200 purchase divided into four payments still costs $200. Miss a payment, and it costs more. Stack three other active plans on top of it, and the combined weight may show up in ways that never appear at the register: more financial stress, slower savings growth, and a harder conversation with a mortgage lender when the time comes.

The tools you use to manage money are only as effective as the awareness you bring to them. BNPL works best as a deliberate, planned choice with a clear repayment path, not as a reflexive tap at checkout because the individual payment looked small.

Quick Reference: BNPL Facts at a Glance

| Question | Answer |

|---|---|

| Is BNPL Always Interest-free? | No. Short Pay in 4 plans often are, but longer plans can carry up to 36% APR. |

| Does BNPL build credit? | Rarely. Most providers do not report on-time payments to the credit bureaus |

| Can BNPL hurt my credit? | Yes. Missed payments can be reported and damage your score. |

| What is a deferred interest plan? | A plan where the lender applies interest retroactively to the original balance if it is not fully paid by a set deadline. |

| Is BNPL safer than a credit card? | Not necessarily. Credit cards carry stronger legal consumer protections. |

| What is the biggest BNPL risk? | Running multiple plans simultaneously and losing visibility over total obligations. |

Final Thoughts: Know What You Are Actually Paying

The phrase “Buy Now, Pay Later” sounds like a favor. In the right circumstances, it can be. But the full cost of any financial decision goes beyond what the checkout screen displays.

Buy Now, Pay Later is a tool with a specific design and a specific business model. When you understand how it works, you are better positioned to use it on your terms. You recognize the late fee structure before it applies to you. You spot the deferred interest clause before it activates. You notice when your active balances are stacking up before the payments start competing with rent.

That kind of awareness is what separates a financial tool from a financial trap. The purchase might still happen, and sometimes it absolutely should. But it should happen because you chose it with complete information, not because four small numbers looked easier than one big one.

That is the real cost of Buy Now, Pay Later. Now you know it.

Watch It Instead

The Money Nudge — YouTube Channel

Prefer watching over reading? Every topic on this blog also comes to life as an animated video on our YouTube channel — where we make money talk even more simply.

Visit Our Channel