Understanding finance does not have to be complicated. Many people hear the word “finance” and immediately think of complex charts, confusing terms, or Wall Street professionals in suits. In reality, finance is something you interact with every single day. Whether you are earning money, saving it, borrowing it, or investing it, you are already participating in finance.

By the end, you will clearly understand the three main fields of finance, how they work, and why they matter in real life. Finance Explained is not about memorizing definitions. It is about understanding how money flows through your life, businesses, and the economy as a whole. Let’s start from the basics and build up step by step.

Prefer to watch instead of read?

Subscribe to The Money Nudge on YouTube for plain-English videos on money, investing, and economic topics.

Table of Contents

What Does Finance Really Mean?

What Is The Real Definition Of Finance?

Read Article →Before we break down the three types, let’s clearly define what finance is in simple terms. Finance is the study and management of money. It focuses on how money is earned, spent, saved, borrowed, and invested over time. The simplest explanation for Finance is: Finance is about making decisions with money. Every financial decision answers one of these questions:

- How much money do I have?

- How should I use it today?

- How should I plan for the future?

- What risks am I willing to take?

Finance Explained also involves time. Money today is not the same as money tomorrow. A dollar today can be saved, invested, or spent. That choice affects your future. This idea is central to all types of finance. Now let’s explore the three main types of finance that shape how money moves in the world.

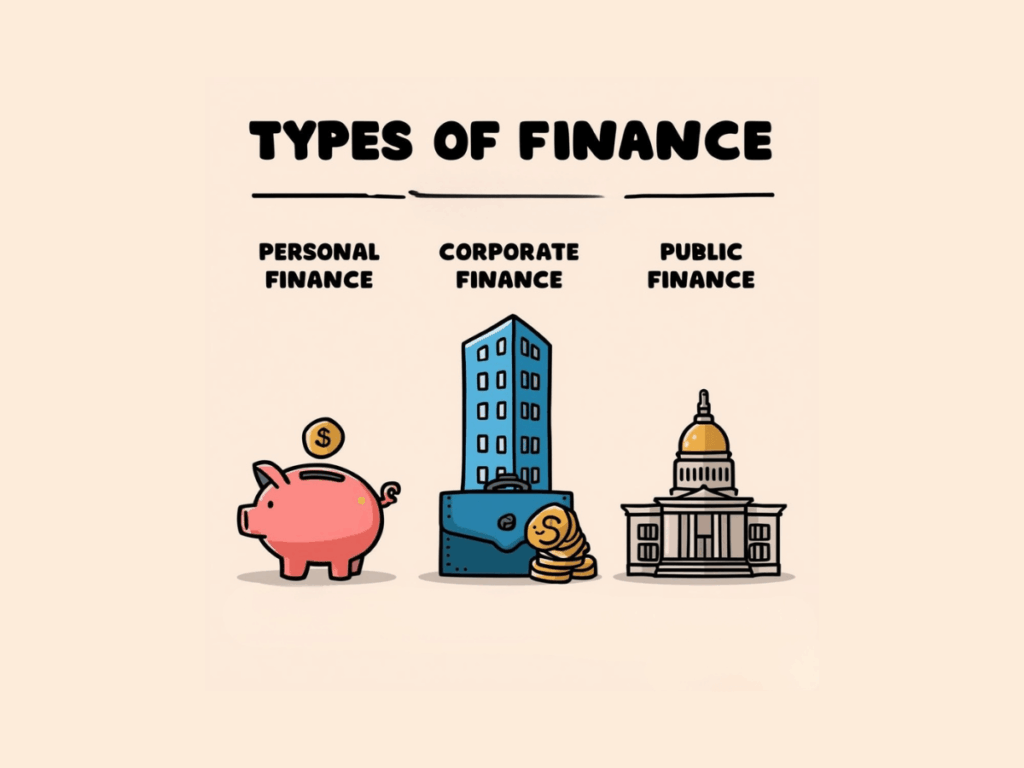

Fields Of Finance

1. Personal Finance

Personal finance focuses on how individuals and households manage their money. This is the type of finance that affects your daily life the most. When people search for ‘Finance Explained,’ this is usually what they want to understand first — not complex corporate deals or stock market theories, but how money works in their paychecks, bills, and bank accounts.

At its core, personal finance begins with income. Income can come from a salary, hourly wages, bonuses, commissions, or even side hustles like freelancing or online sales. Understanding how much money consistently comes in each month is the starting point of financial clarity. Without knowing your real income after taxes and deductions, it is nearly impossible to make sound financial decisions.

From there, expenses come into play. Expenses include rent or mortgage payments, transportation, groceries, utilities, insurance, subscriptions, and everyday spending. Some expenses are fixed and predictable, like rent. Others fluctuate, like entertainment or dining out. The key idea in Finance Explained at a personal level is awareness. When you know where your money is going, you gain control over it.

Saving money is the next essential layer. Saving is not just about putting away whatever is left at the end of the month — because for many people, nothing is left. Instead, strong personal finance habits treat savings as a priority. This could mean building an emergency fund that covers three to six months or even more of living expenses. It could also mean setting aside money for short-term goals, such as a vacation or a home down payment. Saving creates financial stability and reduces stress when unexpected events happen.

Borrowing money is another part of personal finance. Mortgages, student loans, car loans, credit cards, or any type of loan can all be useful tools when managed properly. However, borrowing without understanding interest rates and repayment terms can lead to long-term financial strain. Finance Explained in real life means knowing when debt is strategic — like financing education that increases earning potential — and when it becomes harmful.

Investing for the future completes the picture. Investing allows money to grow over time through compound returns. Retirement accounts, brokerage accounts, and even small monthly contributions to index funds are practical examples. The earlier someone begins investing, the more time works in their favor.

In simple terms, personal finance is about balancing what you earn with what you spend, while intentionally preparing for both emergencies and long-term goals. It is not about being perfect. It is about being proactive instead of reactive. When you truly understand Finance Explained at the personal level, money stops feeling chaotic and starts becoming a tool that works for you instead of against you.

2. Corporate Finance

The focus of Corporate finance is how businesses manage money. While personal finance is about individuals organizing their income and expenses, corporate finance is about companies making financial decisions to grow, compete, and survive over time. The scale is different, but the core idea remains the same: resources are limited, choices have consequences, and money must be managed strategically.

Finance explained in a business context means answering fundamental questions that shape a company’s direction. How should a company raise money? How should it spend that money? How can it maximize profits while managing risk? These are not theoretical questions. They are daily decisions made by executives, financial managers, and business owners.

Every business, from a small local shop to a global corporation, must deal with corporate finance. A family-owned restaurant deciding whether to renovate its dining area is practicing corporate finance. A technology company deciding whether to acquire a competitor is also practicing corporate finance. The difference lies in size, not in principle.

When companies need money, they have several options. They can use profits generated from operations, borrow from banks, or issue shares to investors. Each path carries trade-offs. If a company uses its own profits, it keeps full control but reduces its cash cushion. If it borrows from a bank, it gains immediate funds but must commit to regular interest payments, increasing financial risk. If it issues shares, it avoids debt but gives up partial ownership and future profit claims.

Consider a practical example. Imagine a retail company that wants to open a new location in another city. The expansion is expected to cost $2 million. Corporate finance analysis will project future sales, estimate expenses, and calculate whether the new store is likely to generate returns greater than the cost of capital. The company must evaluate not only potential profit but also risk. What if demand is lower than expected? What if construction costs rise? These projections guide decision-making.

Corporate finance also involves capital budgeting, the process of deciding where to invest company funds. Should the company buy new equipment that increases efficiency? Should it invest in marketing to increase brand awareness? Should it expand into an international market? These decisions are not based solely on optimism. Finance explained at this level involves analyzing expected cash flows and comparing them with the investment’s cost. If the expected return exceeds the required return, the project may move forward.

Risk management is another essential component. Companies face risks from competition, economic downturns, inflation, interest rate changes, and technological disruption. A company heavily dependent on one product may diversify its offerings to stabilize revenue. A business exposed to fluctuating raw material prices might lock in long-term contracts to reduce uncertainty. These are financial strategies designed to protect profitability.

Corporate finance also directly affects employees and consumers. Financially strong companies are more likely to maintain stable jobs, invest in innovation, and offer competitive salaries. Companies under financial pressure may freeze hiring, cut costs, or increase prices. When you see product prices rise or hear about layoffs, corporate finance decisions are often behind those outcomes.

Even if you never run a business, corporate finance influences your investment returns if you own stocks or retirement accounts. The decisions companies make about debt, expansion, and profitability directly affect shareholder value.

Understanding finance explained from a corporate perspective helps you see how strategy, risk, and money connect. It shows that behind every business headline is a financial decision aimed at balancing growth, stability, and long-term value creation.

3. Public Finance

Public finance focuses on how governments manage money. While personal finance applies to individuals and corporate finance applies to businesses, public finance applies to entire nations, states, and municipalities. It examines how governments collect revenue, how they allocate resources, and how those decisions influence economic stability and social well-being. In simple terms, public finance is about how a country funds its operations and invests in its future.

Finance explained at the public level begins with revenue. Governments primarily raise money through taxation. Income taxes are collected from individuals and businesses based on earnings. Sales taxes are collected from goods and services purchased by consumers. Property taxes are collected from real estate ownership. Beyond that, governments also generate revenue through corporate taxes, payroll taxes, import tariffs, and a range of administrative fees. Each of these tax policies reflects a broader economic philosophy regarding fairness, economic growth, and the redistribution of resources within society.

When you receive a paycheck and see deductions for federal or state taxes, you are directly participating in public finance. Those funds are pooled together and used to finance public services. Education systems, public universities, healthcare programs, national defense, law enforcement, transportation infrastructure, and social assistance programs all rely on government revenue. Roads are built and maintained through public funds. Emergency services respond to crises using taxpayer resources. Public finance, therefore, touches daily life more than many people realize.

Government spending decisions are complex because resources are limited. If a government increases healthcare funding, it may need to reduce spending elsewhere or raise additional revenue. Allocating funds to infrastructure projects may stimulate economic growth, but it could also increase short-term budget deficits. Finance explained in this context highlights trade-offs on a national scale. Policy makers must weigh economic priorities, social needs, and political realities.

Deficits occur when governments spend more than they collect in revenue during a fiscal year. To cover this gap, governments borrow money by issuing bonds to investors. This borrowing creates government debt. Debt itself is not automatically negative. In many cases, governments borrow to finance long-term investments, such as highways, energy systems, and research initiatives, that can increase productivity for decades. If those investments generate economic growth, future tax revenues may offset the borrowing.

However, excessive or poorly managed debt can create challenges. High debt levels will probably lead to higher interest payments, which consume a larger portion of the national budget. If investors lose confidence, borrowing costs may rise. Public finance, therefore, includes managing debt responsibly and ensuring long-term sustainability.

Public finance also affects inflation and interest rates. Government spending and borrowing can influence the overall money supply and economic demand. During economic downturns, governments may increase spending to stimulate growth. During periods of high inflation, they may reduce spending or adjust taxes to stabilize prices.

Understanding finance explained at the public level helps you interpret economic news and policy debates with greater clarity. When politicians discuss tax reforms, stimulus packages, or budget cuts, they are engaging in public finance decisions. These choices shape economic stability, job markets, and long-term prosperity.

How the Three Fields of Finance Work Together

The three main fields of finance — personal, corporate, and public — do not operate in isolation. They are deeply interconnected, constantly influencing and reinforcing one another. While each area has its own focus and decision-makers, money ultimately flows between individuals, businesses, and governments in a continuous and dynamic cycle.

At the most basic level, individuals work for businesses. In exchange for their time and skills, they receive wages or salaries. That income serves as the foundation for personal finance decisions. People use their earnings to pay rent or mortgages, buy groceries, invest for retirement, and spend on goods and services. When individuals spend money, businesses generate revenue. That revenue allows companies to pay employees, invest in expansion, purchase equipment, and distribute profits to shareholders.

Businesses, in turn, participate in public finance. They pay corporate taxes on profits, payroll taxes on employee wages, and sales taxes collected from customers. This revenue funds public services, including infrastructure, education, healthcare, and public safety. Without stable businesses generating income and paying taxes, government revenue would decline significantly.

Governments also support both individuals and companies. Roads, bridges, ports, and digital infrastructure allow businesses to transport goods and operate efficiently. Public education systems prepare the workforce that companies depend on. Property rights and enforceable contracts are protected by legal systems, both of which are essential to economic stability. Even central banking policies influence interest rates, affecting how individuals borrow for homes and how businesses finance expansion.

Consider a practical example. A technology company decides to expand operations and hire 200 new employees. That is a corporate finance decision involving capital allocation and growth strategy. Those new employees now earn salaries, strengthening their personal finances, and on top of that, they support local businesses by spending their money in the local community. The company pays payroll taxes and corporate taxes, contributing to public finance. The government may use those funds to improve local infrastructure, which further benefits businesses and residents. The cycle continues.

When individuals invest in retirement accounts that include stocks, they are also connecting personal finance to corporate finance. Their savings provide capital that companies use to innovate and grow. If those companies succeed, investors benefit through dividends or rising stock prices. At the same time, governments regulate financial markets to protect investors and maintain stability, tying public finance into the system once again.

Finance explained clearly shows that these three areas are not separate worlds. They are parts of a single economic ecosystem. A disruption in one area often affects the others. For example, during an economic recession, businesses may reduce hiring or lay off workers. That impacts personal income and spending. Lower spending reduces business revenue, thereby decreasing tax collections for governments. Public budgets may tighten, leading to reduced services or increased borrowing. The interconnection becomes visible.

Understanding how these fields work together gives you a broader perspective. Instead of viewing financial decisions as isolated events, you begin to see patterns and relationships across the entire economy.

Why Understanding Finance Explained Is So Important

Many financial problems arise not simply because people lack money, but because they lack clarity. Without understanding how money and decisions create long-term consequences, it is easy to fall into reactive behavior. Finance explained empowers you to think strategically rather than emotionally.

Understanding personal finance gives you control over your daily decisions. You recognize the importance of budgeting, building emergency savings, and managing debt responsibly. You become more intentional about investing for the future rather than relying on guesswork.

When you understand corporate finance, you are better equipped to evaluate companies as an employee or investor. You can analyze whether a business is financially stable, growing responsibly, or taking excessive risks. This knowledge helps you make smarter investment choices and understand job market trends. If a company is highly leveraged or struggling with cash flow, you may recognize warning signs earlier.

When you understand public finance, you can interpret policy decisions with greater insight. Discussions about tax reforms, government spending, budget deficits, and national debt become clearer. Instead of reacting to headlines, you can evaluate how policies might influence economic growth, inflation, or employment.

Ultimately, finance explained is about awareness. It connects your paycheck to corporate earnings and government policy. It helps you see how economic decisions ripple outward. When you understand these connections, you are not just managing money — you are understanding the system that shapes opportunity, stability, and growth in everyday life.

Final Thoughts: Finance Explained for Everyday Life

Finance does not belong only to experts. It belongs to everyone. The three main types of finance help explain how money moves through your life, businesses, and society. Personal finance focuses on your money. Corporate finance focuses on business money. Public finance focuses on government money. Together, they form the foundation of the financial world. This Finance Explained guide shows that finance is not about complexity. It is about understanding choices, planning ahead, and using money as a tool to build stability and opportunity. Once you understand the basics, finance stops being scary and starts becoming empowering. And that is the real goal of Finance Explained.

Watch It Instead

The Money Nudge — YouTube Channel

Prefer watching over reading? Every topic on this blog also comes to life as an animated video on our YouTube channel — where we make money talk even more simply.

Visit Our Channel