Most people do not set out to stay in debt. The plan, in most cases, is simple: charge the purchase, make the credit card minimum payment for now, and catch up later. It feels manageable. The bank even tells you the minimum payment right there on the statement, as if that number were the amount you owe. But that number is not what you owe. It is the least the bank requires you to pay before adding more interest to everything you already carry. The distance between those two things — what you owe and what you pay — is where the real cost of a credit card lives.

This article is not about shaming anyone for carrying a balance. Credit cards are a normal part of modern financial life, and situations change. This article is about the math. Because once you see how the numbers actually work — what a $2,000 balance truly costs when you pay only the minimum, and what a $5,000 balance costs over time — the minimum payment line on your statement starts to look very different.

Watch the Money Nudge YouTube Video about the definition of Finance:

Prefer to watch instead of read?

Subscribe to The Money Nudge on YouTube for plain-English videos on money, investing, and economic topics.

Table of Contents

What a Minimum Payment Actually Is

Before getting into the numbers, it is worth understanding what the credit card minimum payment actually represents. Banks calculate it in different ways, but the most common method is either a flat dollar amount (often $25 or $35) or a small percentage of the outstanding balance, whichever is greater. That percentage is typically somewhere between 1% and 2% of the total balance.

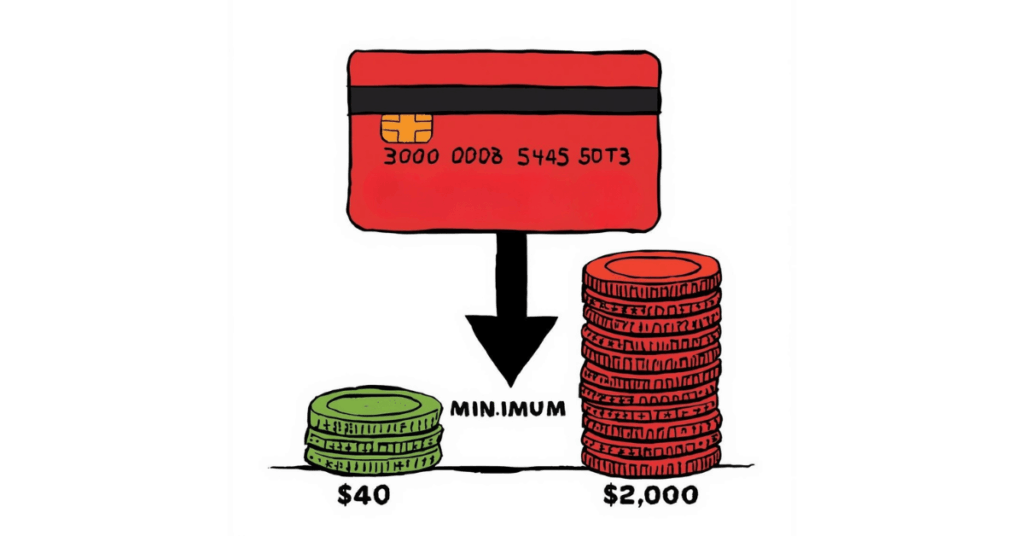

On a $2,000 balance at 2%, your minimum payment would be $40. On a $5,000 balance, it would be $100. Those numbers feel reasonable, especially compared to the total you owe. That is precisely the problem. The minimum payment is designed to keep the account in good standing, not to get you out of debt. It is the floor, not the target.

The deeper issue lies in how credit card interest compounds against a slowly moving balance. Each month, the lender calculates interest on the unpaid balance, and that charge is applied before any payment reduces the principal. A minimum payment covers that interest charge first. What is left over chips away at the actual debt, and that leftover amount tends to be surprisingly thin. The minimum payment also decreases as the balance declines, further stretching the repayment timeline. The debt shrinks, but it shrinks at a pace that can keep someone in repayment for the better part of a decade.

What is interest rate? A Simple and Clear Explanation

Read Article →The $2,000 Balance: A Story in Numbers

Take a $2,000 credit card balance. This is not an unusual amount. It could be a car repair, a medical bill, a few months of groceries during a difficult stretch, or a holiday season that got away from someone. The average credit card interest rate in the United States currently sits above 20% annually. For this example, a rate of 20% APR will be used, which is realistic for many cardholders.

At 20% APR and a minimum payment of 2% of the balance (with a $25 floor), the minimum on a $2,000 balance is $40 per month. That sounds fine. But here is the full picture.

Paying only the minimum each month on a $2,000 balance at 20% APR will take approximately nine years and six months to pay off compFinance Definition: What It Really Means and Why It Matters in Everyday Lifeletely. Over that period, you will pay roughly $1,900 in interest alone. That means the $2,000 you originally spent ends up costing you close to $3,900.

Read that again. A $2,000 balance — paid on time, never missed, always meeting the minimum requirement — nearly doubles in total cost. The item or experience you charged is paid for twice. And because the minimum payment shrinks as the balance shrinks, the process slows down even further. There are months near the middle of that repayment window when only a few dollars of the minimum payment are applied to principal.

APR: What Is It and Why It Matters More Than You Think

What if I tell You that Interest Rates are not everything?

Read Article →The $5,000 Balance: The Weight Gets Heavier

Now consider a $5,000 balance at the same 20% APR. This is the kind of balance that builds over time — not necessarily from one large purchase, but from months of carrying a smaller balance that was never fully cleared. A few hundred here, a few hundred there, and before long, the statement reads five figures.

Apply the same 2% minimum to a $5,000 balance, and the opening payment is $100 per month. Running that figure through the same rate and method produces a result that catches most people off guard. The debt does not clear for roughly 12 to 13 years, and the lender collects somewhere between $5,500 and $6,000 in interest along the way.

That means a $5,000 debt costs more than $10,000 by the time it is gone. The interest alone exceeds the original balance. Every dollar of that original $5,000 is paid back, and then an additional $5,000-plus is handed to the lender on top of it. This is not a worst-case scenario. This is standard minimum payment math at a common interest rate.

The reason the numbers grow so dramatically comes down to how credit card interest is calculated. Interest compounds monthly, meaning the bank calculates interest on the balance each month. When you pay only the minimum, the balance does not shrink fast enough to reduce next month’s interest charge meaningfully. The debt persists, the interest keeps accumulating, and the repayment timeline stretches far beyond what most people expect when they first swipe the card.

Why the Minimum Payment Feels Like Enough

There is a psychological dimension to this that is worth naming honestly. The minimum payment is a responsible choice because it is the number the bank puts in front of you. It shows up prominently on the statement. Paying it on time means no late fees, no penalty rate, and no negative mark on a credit report. The system rewards paying the minimum. That reward signal — the feeling of handling a bill correctly — can obscure the slower, quieter cost of carrying the balance.

There is also a cognitive bias called present bias at work here. Humans tend to weigh immediate costs more heavily than future ones. Paying $200 toward a $5,000 balance this month feels painful right now. Paying $100 feels manageable. The additional $1,000 or $2,000 in interest that will accumulate over the next decade feels abstract. The brain has difficulty treating a cost that arrives twelve years from now with the same urgency as a cost that arrives this month. That gap between present pain and future cost is what the minimum payment structure quietly exploits.

Understanding this does not make anyone foolish for having used a minimum payment strategy. It makes the situation clearer. The feeling of manageability is real. The math, however, does not care about feelings.

How Finance Impacts Your Daily Life?

Read Article →The Real Cost of Minimum Payments: A Side-by-Side Look

The two scenarios side by side make the cost of minimum payments hard to ignore. Both rows use a 20% APR, a 2% declining minimum payment, and a $25 floor for the calculation.

| Balance | Monthly Start Payment | Years to Pay Off | Total Interest Paid | Total Amount Paid |

|---|---|---|---|---|

| $2,000 | ~$40 | ~9.5 Years | ~$1,900 | ~$3,900 |

| $5,000 | ~$100 | ~12.5 Years | ~$5,700 | ~$10,700 |

These are not extreme examples. They are not based on predatory rates far above the market average. They reflect what ordinary balances at ordinary interest rates cost when the only payment made each month is the minimum. The numbers speak for themselves without requiring any embellishment.

What Happens When You Pay More

The contrast between paying the minimum and paying even slightly more is dramatic. This is not to suggest any particular amount — every financial situation is different — but the math illustrates why the size of the payment matters enormously.

On the same $2,000 balance at 20% APR, consider what changes if the monthly payment is fixed at $80 instead of the declining minimum. The payoff time drops to roughly 28 months, and the total interest paid falls to around $300. The difference between a $40 starting payment and an $80 fixed payment is $1,600 in interest saved and more than seven years of debt cleared.

On the $5,000 balance, fixing the payment at $200 per month instead of the declining minimum reduces the payoff time to approximately 32 months and cuts total interest to around $1,400. Compared to the minimum-only path, that is more than $4,000 in savings and nearly ten fewer years of carrying the debt.

The point here is not that doubling the payment is always possible. The point is that the relationship between payment size and total cost is not linear — small increases in the payment amount create outsized reductions in interest paid. The minimum payment is the most expensive way to repay a credit card balance. Any amount above it accelerates the exit from debt.

What the Credit Card Statement Does Not Tell You

U.S. law requires lenders to print a specific warning on every credit card statement. That warning projects the total repayment time and total cost if the cardholder pays only the minimum each month. Most people have noticed that box at some point. Very few stop to read it carefully, because the minimum payment amount is larger and more immediate, and the warning tends to sit quietly in a corner of the page.

The language in that box is not hypothetical. It is the actual math applied to the actual balance at the actual interest rate. When it says “13 years” or “total cost of $10,400,” those are real projections based on real numbers. The fact that this disclosure exists as a legal requirement reflects how significant the gap between minimum payment cost and full payoff cost actually is. It was considered serious enough to be mandated by law.

Most people glance past it. The minimum payment amount is larger on the page, easier to act on, and tied to a concrete due date. The warning box tends to sit quietly in a corner, easy to skip over when life is busy and the bill needs to be paid.

Credit Card Interest: How the Rate Shapes Everything

The 20% APR used throughout this article is a reasonable benchmark for illustration, but interest rates vary. Some cards charge 15%, others charge 25% or more. The rate matters because it determines how fast the balance grows between payments.

Credit card interest is charged at an annual rate and applied to the balance each month. A 20% APR translates to a monthly charge of roughly 1.67% — the annual rate divided by 12 billing cycles. On a $5,000 balance, the monthly charge is approximately $83 before a single payment is applied. A $100 minimum payment arrives, $83 of it cancels the interest, and the remaining $17 actually reduces the debt. The balance drops by $17. The lender collects $83. That is the arithmetic of a minimum payment at 20% APR.

At a higher rate, say 25% APR, the monthly interest rate climbs to about 2.08%. On $5,000, that is $104 in interest accruing in month one. A $100 minimum payment does not even cover the interest — the balance actually grows despite making a payment. This situation is sometimes called a negatively amortizing loan, and it can trap cardholders in a balance that increases even when they pay on time every month.

Understanding how the rate connects to monthly interest charges is one of the most important pieces of financial literacy a person can have. The rate on a credit card is not a background detail. It is the engine driving the total cost of carrying any balance.

The Invisible Opportunity Cost

There is another dimension to paying the minimum on a credit card that rarely gets discussed: what that money could be doing instead. Every dollar paid in credit card interest is a dollar that cannot be saved, invested, or used for anything else. Over the nine-plus years it takes to pay off a $2,000 balance through minimum payments, the $1,900 paid in interest represents money that left permanently — not toward an asset, not toward a financial goal, not toward anything with lasting value.

If those same dollars had been directed toward a savings vehicle earning even a modest return, the total would compound over time into something meaningful. This is not to suggest that avoiding interest is always the right financial priority for every person in every situation. It is to make visible a cost that the minimum payment structure tends to obscure. The interest paid on a credit card is a real transfer of wealth from the cardholder to the lender, and it happens slowly enough that it rarely feels dramatic. The math, however, adds up to thousands of dollars over time.

Everything You Should Know About The Opportunity Cost

Read Article →Common Scenarios Where This Plays Out

The abstract becomes more concrete when mapped onto actual situations. Consider a few common patterns.

The holiday balance: A $1,500 balance accumulated in December through gifts, travel, and celebrations. The intention is to pay it off by March. But in February, an unexpected expense arises, and the minimum becomes the default. By the following December, the balance has barely moved, and another holiday season is about to add to it. A one-time seasonal expense becomes a multi-year debt carried at 20% interest.

The emergency balance: A $3,000 car repair or medical bill is charged to a credit card because there is no other option at the moment. The plan is to tackle it aggressively once things stabilize. Things stabilize, but the minimum payment is already set up on autopay, and the debt is being handled. Three years later, over $1,500 in interest has been paid on a bill that never grew, never changed, but never fully left.

The slow accumulation: No single large purchase; just $200 to $400 in monthly charges that never fully clear. Over two or three years, the balance climbs to $4,000 or $5,000. The minimum payment has been made consistently and on time throughout. The credit score looks fine. But the balance has been costing hundreds of dollars in interest per year the entire time.

Each of these scenarios is recognizable because it is common. The minimum payment is not a crisis. It is a slow drain, and slow drains are often the hardest to notice.

How to See Your Balance Differently

There is a reframe that can change how a credit card balance feels. Instead of reading the balance as a number to manage, treat it as a monthly cost. At 20% APR, a $2,000 balance costs approximately $33 per month in interest. A $5,000 balance costs approximately $83 per month. Those monthly interest charges are not building equity, not funding anything, not purchasing anything. They are simply the fee for carrying the balance forward one more month.

Framing the interest charge as a recurring monthly cost — like a subscription that produces nothing — tends to make the balance feel less abstract. Nobody would cheerfully pay $83 per month for a service that delivered zero value. But that is roughly what a $5,000 credit card balance at 20% APR costs every single month it is carried.

The point of this reframe is not to make the reader feel bad about a balance. It is to make the ongoing cost of that balance tangible. Keeping an account in good standing and keeping debt cheap are separate outcomes. The minimum payment achieves the first one. It does nothing toward the second. Credit card statements present both numbers — the balance and the minimum due — without making that gap obvious.

What This Means for Long-Term Financial Health

The weight of carrying a high-interest balance over many years reaches beyond the interest itself. Debt carried over a long period shapes financial behavior in ways that compound over time. It limits the amount available to save or invest each month. It can create a persistent sense of financial instability even when income is stable. It occupies mental bandwidth that might otherwise go toward building something rather than managing a liability.

None of this is permanent. A balance paid off, even slowly, and eventually reaches zero. The trajectory matters. Moving from minimum-only payments toward higher fixed payments, even gradually, changes the long-term cost dramatically. The math rewards even modest increases in payment size far more than most people expect.

The goal of understanding the cost of minimum payments is not to generate anxiety. It is to make an invisible cost visible. Most people who carry a balance are not careless with money. They are managing competing demands with limited resources, making trade-offs in real time. The problem is not the decision — it is making a decision without seeing the full math behind it.

Final Thoughts: The Number That Matters Most

The minimum payment due is printed clearly on every statement. It is easy to find, easy to act on, and easy to feel good about paying. The total cost of only paying that amount, however, is buried in a disclosure box or requires a separate calculation that most people never run.

A $2,000 balance can cost $3,900. A $5,000 balance can cost more than $10,000. Those totals are not the result of missed payments or financial irresponsibility. They are the result of paying exactly what the bank asked, month after month, while interest compounded quietly in the background. The credit card minimum payment is not a repayment plan. It is the entry fee for staying in debt.

Understanding that distinction is one of the most practical pieces of financial awareness a person can carry. It does not require a spreadsheet or a finance degree. It requires seeing the minimum payment for what it is: the floor, not the ceiling, and certainly not the way out.

Watch It Instead

The Money Nudge — YouTube Channel

Prefer watching over reading? Every topic on this blog also comes to life as an animated video on our YouTube channel — where we make money talk even more simply.

Visit Our Channel