Most small business owners reach a point where the numbers stop making sense. Revenue looks steady. The workload feels consistent. Yet month after month, the total cost of running the business swings in ways that seem random. One month, expenses are manageable. The next month, they spike without warning. The business did not change overnight, but the bank balance tells a different story. That frustrating gap between expectation and reality almost always comes down to one overlooked distinction: the difference between fixed expenses and variable expenses.

Understanding variable expenses and how they differ from fixed costs is not an advanced accounting concept reserved for finance professionals. It is one of the most practical skills any business owner can develop, regardless of industry, business size, or experience level. Once you can identify which costs stay the same and which ones shift with your activity level, pricing decisions get sharper, cash flow becomes more predictable, and growth stops feeling like a gamble. This article walks through that distinction from the ground up, using examples of real business scenarios that apply whether you run a food truck or a freelance design studio.

Watch the Money Nudge YouTube Video about the definition of a Recession:

Prefer to watch instead of read?

Subscribe to The Money Nudge on YouTube for plain-English videos on money, investing, and economic topics.

Table of Contents

What Fixed Expenses Are and Why They Stay the Same

Fixed expenses are the costs a business pays regardless of how much work it does or how many products it sells. These costs do not change based on business activity. They show up every single month at roughly the same amount, whether the business had its best month ever or its slowest week in years.

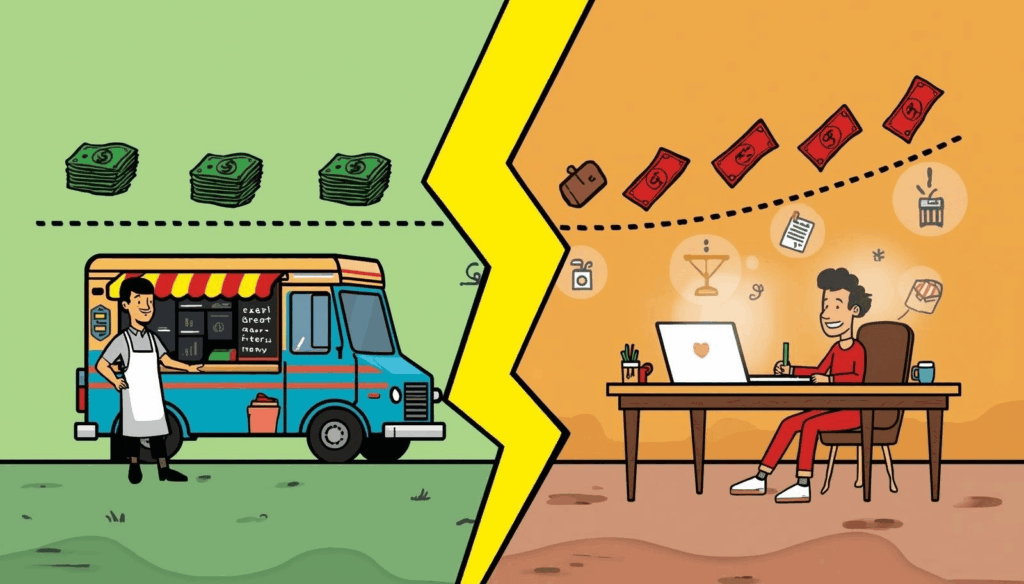

For a food truck owner named Marco, fixed expenses include the monthly payment on his truck, the insurance premium covering his vehicle and liability, the commercial kitchen rental where he preps ingredients each morning, and the software subscription he uses to manage orders. None of these costs go up when Marco sells 300 tacos in a day instead of 150. None of them go down when it rains, and he sells only 50. They remain constant.

For a freelance graphic designer named Priya, fixed expenses look different but follow the same pattern. Her monthly coworking space membership costs the same whether she takes on five clients or one. Her Cloud subscription renews at the same rate regardless of how many projects she delivers. Her internet bill and her professional liability insurance stay flat from month to month. These costs exist simply because the business exists, not because it produced anything specific.

The defining feature of fixed expenses is their predictability. A business owner can look at last month’s costs and know, with high confidence, what next month’s costs will be. That predictability is valuable because it creates a baseline. It tells you the minimum revenue the business must generate to keep the doors open before a single product ships or a single invoice is issued.

Everything You Should Know About The Opportunity Cost

Read Article →What Variable Expenses Are and How They Move With Your Business

Variable expenses behave oppositely. These are costs that rise and fall in direct proportion to business activity. When the business does more, variable expenses increase. When the business slows down, variable expenses decrease. They are tied directly to production, delivery, or the volume of work the business performs.

Back at Marco’s food truck example, variable expenses include the ingredients he buys each week, the disposable containers and napkins he uses, the truck’s fuel when he drives to different locations, and the credit card processing fees charged for every transaction. On a busy festival weekend, Marco might spend three times more on tortillas, meat, and produce than he spends during a quiet Tuesday lunch shift. His ingredient costs are variable expenses because they scale with the number of meals he serves.

For Priya, variable expenses show up differently. When she takes on a branding project that requires custom stock photography, the cost of those image licenses is a variable expense. When a client requests printed mockups, the printing and shipping costs are variable. If she hires a freelance copywriter to handle the text for a website project, that subcontractor’s fee is a variable expense tied to that specific job. During months when Priya takes on larger or more complex projects, her variable expenses climb. During quieter months, they shrink.

The key characteristic of variable expenses is that they only exist because a specific business activity triggered them. No sales means no packaging costs for Marco. No client projects means no stock photo purchases for Priya. Variable expenses are direct costs of doing business at a particular volume and flex with every change in that volume.

Learn The Difference Between Finance Vs. Accounting

Read Article →Why the Distinction Between Fixed Expenses and Variable Expenses Matters for Pricing

One of the most immediate and practical reasons to understand the split between fixed and variable expenses is pricing. Every product or service a business sells must generate enough revenue to cover both types of costs and still leave room for profit. Getting the math wrong on either side leads to pricing that looks profitable on the surface but quietly bleeds money underneath.

Marco sells his signature tacos for $5 each. His ingredient and packaging cost per taco, which is a variable expense, runs about $1.80. That leaves $3.20 per taco. A quick look at that margin might suggest Marco is doing well. But that $3.20 does not represent profit. It represents contribution margin, which is the amount each sale contributes toward covering fixed expenses. Marco still needs to pay for his truck, insurance, kitchen rental, and subscriptions before he earns a single dollar of actual profit.

If Marco’s total fixed expenses run $4,500 per month, he needs to sell at least 1,407 tacos every month to break even. That is $4,500 divided by the $3.20 contribution margin per taco. Every taco sold after number 1,407 generates real profit. Every taco sold below that number means Marco is losing money, even though each sale appears to carry a healthy margin.

Priya faces the same math with a different structure. If she charges $3,000 for a brand identity package and her variable costs for that project total $400 in stock images, printing, and a subcontracted illustration, her contribution margin is $2,600 per project. With monthly fixed expenses of $2,100 for her coworking space, software, insurance, and phone, Priya needs to complete at least one full project per month to break even. A second project in the same month produces nearly pure profit, with only the variable costs tied to that specific job deducted.

Without separating fixed and variable expenses, neither Marco nor Priya could set prices with any confidence. They would be guessing, and guessing at pricing is one of the fastest ways for a small business to run into cash flow trouble.

Cash Flow: Everything You Need To Know To NOT Blow Up Your Business

Read Article →How Fixed and Variable Expenses Behave Differently During Growth and Slowdowns

The distinction between these two categories becomes even more important when a business grows or contracts. Fixed and variable expenses respond to changes in business volume in fundamentally different ways, and understanding that difference determines whether growth actually increases profit or increases stress.

As Marco’s food truck gets busier, his variable expenses rise in proportion. More customers mean more ingredients, more packaging, more fuel, and more transaction fees. But his fixed expenses stay flat. His truck payment does not increase because he sold more tacos. His insurance premium does not rise because the line at his window got longer. This is the power of fixed costs during growth: they get spread across more units. Marco’s fixed expense per taco declines as he sells more, so his profit margin per taco actually improves with volume.

The reverse is also true, and it is where many business owners get caught off guard. During a slow month, Marco’s variable expenses decrease because he buys fewer ingredients and processes fewer transactions. But his fixed expenses remain the same. The truck payment is still due. The insurance premium has not changed. The kitchen rental fee stays constant. With fewer tacos sold, each taco now carries a heavier share of those fixed costs, and the margin per unit shrinks. A slow enough month means Marco cannot cover his fixed expenses at all, even if every single taco he sells is individually profitable.

Priya experiences the same dynamic. Adding a third or fourth client in a busy month increases her variable costs, like additional stock photos or subcontractor fees. Still, her coworking membership and software subscriptions remain the same. More projects spread those fixed costs across a larger revenue base, boosting her overall profitability. But a month with zero client projects means Priya still owes the full amount of her fixed costs, with no revenue to offset them.

This is why understanding fixed and variable expenses is essential for planning around seasonal patterns, economic downturns, and other periods when revenue drops. A business owner who understands the fixed cost floor can prepare for slow periods by building a cash reserve to cover non-negotiable monthly expenses.

What Happens When a Business Owner Confuses Fixed and Variable Expenses

The consequences of misunderstanding which expenses are fixed and which are variable show up in several common and costly ways. The most damaging is underpricing, and it happens more often than most business owners realize.

A business owner who lumps all costs together into a single “expenses” number loses the ability to calculate an accurate break-even point. Without knowing the contribution margin, pricing becomes a matter of intuition or competitor imitation rather than math. Marco might see a competitor selling tacos for $4 and decide to match that price, unaware that his fixed-cost structure requires a $5 price to survive. Priya might underbid a branding project because she only considered her variable costs and forgot that her fixed monthly overhead still needs to be covered by every project she takes on.

The second consequence is poor cash flow forecasting. A business owner who treats all expenses as variable might expect costs to drop during slow months. When they do not, because fixed expenses remain constant, the business runs short on cash at exactly the moment it can least afford to. Marco might assume that a slow January will be cheap because he is buying fewer ingredients. He forgets that his truck payment, insurance, and kitchen rental total $4,500 regardless of how many tacos he sells. That surprise gap between expected and actual costs is what pushes many small businesses into emergency borrowing or credit card debt.

The third consequence affects growth decisions. A business owner who does not understand the fixed cost advantage of scaling might hesitate to invest in growth because they assume every increase in revenue comes with a proportional increase in costs. In reality, growing revenue while holding fixed costs steady is one of the most reliable ways to improve profitability. Adding a second service window or extending his hours costs very little in additional fixed expenses but could dramatically increase his contribution margin by serving more customers.

Confusing these two categories does not just create accounting headaches. It leads to real decisions that cost real money. Prices get set too low. Slow months create unnecessary panic. Growth opportunities get passed over. All of these problems trace back to one root cause: not knowing which costs move and which ones stay put.

How to Identify Fixed and Variable Expenses Inside a Business

Walking through the process of sorting expenses into these two categories is simpler than most business owners expect. The method involves a straightforward question for each line item on the monthly expense list: Does this cost change when business activity changes?

Consider Marco’s food truck as a complete example. Here is how each of his major expenses sorts out.

His truck loan payment is $1,200 per month regardless of sales volume. That is a fixed expense. His commercial liability insurance costs $350 per month, billed at that rate year-round. Fixed. His commercial kitchen rental costs $800 per month, with no usage adjustment. Fixed. His point-of-sale software subscription costs $75 per month. Fixed. His business cell phone plan costs $85 per month. Fixed. Marco’s total monthly fixed expenses come to $2,510.

Now for the costs that move. Marco’s food and ingredient purchases run anywhere from $2,000 in a slow month to $5,500 during a busy festival season. Variable. His disposable serving containers, napkins, and utensils cost between $200 and $600, depending on volume. Variable. His fuel costs range from $150 to $400 based on how many locations he visits and how far apart they are. Variable. His credit card processing fees, charged as a percentage of each transaction, fluctuate with total sales revenue. Variable.

Priya can run the same exercise. Her coworking membership at $400 per month is fixed. Her Adobe Creative Cloud at $55 per month is fixed. Her professional liability insurance at $125 per month is fixed. Her domain hosting and portfolio website are fixed at $30 per month. Her total fixed expenses come to $610 per month.

Her variable expenses include stock photo and font license purchases, which range from $0 to $300 depending on project needs. Subcontractor payments vary from $0 in months she handles everything solo to $1,500 or more when she brings in a copywriter or illustrator. Printing costs for physical deliverables fluctuate with each project scope. Shipping costs for mailed materials depend entirely on client requirements.

The sorting process takes most business owners less than an hour with their bank statements or bookkeeping software open. The result is a clear picture of the cost floor, which is the total fixed expenses, and a realistic range for variable costs at different levels of business activity.

Semi-Variable Expenses: The Costs That Do Not Fit Neatly

Some business expenses do not fall cleanly into one category. These are called semi-variable expenses, and recognizing them prevents confusion when certain line items seem to belong in both columns at once.

A semi-variable expense has a fixed base cost plus a variable component that changes with usage. Marco’s cell phone plan offers a practical example. His base plan costs $85 per month, which is fixed. But during busy months, he uses significantly more data for processing mobile payments, running his GPS-based location service, and posting to social media. If his plan charges overage fees or he upgrades his data tier during peak season, the total phone cost exceeds the base amount. The $85 base is fixed. The overage or upgrade is variable. The total is semi-variable.

Priya encounters semi-variable costs with her internet service. The base plan for her coworking space is included in her membership. Still, she also maintains a home internet connection for evening and weekend work. The base subscription is fixed, but when she works on large file transfers or video-heavy projects, she occasionally needs to upgrade her speed tier for a month. The base cost remains constant, while usage-driven upgrades fluctuate.

Utilities are another common semi-variable expense for businesses that operate in physical spaces. A retail shop pays a base charge for electricity regardless of usage. Still, the total bill rises during months with heavier lighting needs, additional heating or cooling, or extended operating hours. The base charge is fixed. The consumption-driven portion is variable.

For practical purposes, most small business owners can handle semi-variable expenses by splitting them into their fixed and variable components. Assign the base amount to the fixed column and estimate the average variable portion for the variable column. This approach keeps the overall cost picture accurate without overcomplicating the exercise.

Connecting Cost Awareness to Smarter Business Decisions

Understanding the split between fixed and variable expenses informs almost every important business decision beyond pricing. It informs hiring, expansion, cost-cutting, and even the decision to shut down during a slow period rather than operate at a loss.

When Marco considers hiring a part-time employee to help during busy shifts, he can evaluate that decision through the lens of fixed and variable expenses. A part-time employee paid by the hour is a variable expense because the cost scales with the hours worked. If Marco only schedules extra help during peak service times, he adds labor cost only when revenue is also higher. If he were to hire a salaried employee instead, that payroll becomes a fixed expense, due every pay period regardless of how many tacos the business sells. The choice between hourly and salaried has real implications for Marco’s cost structure and his ability to weather slow periods.

When Priya considers upgrading from a shared coworking desk to a private studio, she is evaluating an increase in fixed expenses. That higher rent will be due every month, whether she books five clients or zero. She needs to honestly assess whether her average revenue supports the higher fixed-cost floor, or whether the upgrade puts her in a position where a single slow month creates a cash crisis.

Cost-cutting decisions also benefit from this framework. A business owner looking to reduce expenses during a downturn gets more strategic results by focusing on variable expenses first, since those reductions are proportional and immediate. Cutting fixed expenses is harder because those commitments often involve contracts, leases, or subscriptions with cancellation penalties. Knowing which expenses fall into which category allows a business owner to prioritize cuts that take effect quickly without triggering penalties or disrupting core operations.

Seasonal planning becomes more precise as well. A business that earns most of its revenue during six months of the year needs to build reserves large enough to cover fixed expenses during the other six. Marco, who operates his food truck year-round but sees a significant dip in winter, can calculate exactly how much cash reserve he needs by multiplying his monthly fixed expenses by the number of slow months he expects. His variable expenses will naturally decrease during the slow season, but the fixed costs will not budge.

Even the decision to temporarily close during an extremely slow period involves this analysis. If revenue drops below the point where it covers even the variable cost of each sale, every transaction actually loses money. At that point, closing temporarily and paying only fixed expenses might be less expensive than staying open and losing money on every sale while still paying those same fixed costs.

Building a Stronger Business With Better Cost Awareness

The distinction between fixed and variable expenses is not a theoretical exercise. It is one of the most useful frameworks a business owner can carry into every financial conversation, every pricing review, and every growth decision. It transforms vague feelings about “expenses being too high” into specific, actionable categories that respond to different strategies.

Fixed expenses are the minimum costs required to keep the business alive. Variable expenses define the cost of doing business at a specific volume. Together, they paint a complete picture of where money goes and how revenue needs to flow to keep the operation sustainable. A business owner who understands this split can price products and services with confidence, plan for slow periods without panic, evaluate growth opportunities with clarity, and cut costs strategically when the situation demands it.

Marco and Priya operate in completely different industries with completely different cost structures. Yet both benefit from the same simple skill: knowing which costs move and which costs stay. That knowledge does not require an accounting degree or a finance background. It requires a single honest look at the monthly expense list and a single consistent question applied to every line item. Does this cost change when business activity changes? The answer sorts every expense into its proper category. It provides the business owner with a foundation for smarter future decisions.

The goal is not to eliminate all variable expenses or to avoid fixed costs entirely. Both are essential to running a business. The goal is to understand each category well enough to make intentional choices rather than reactive ones. That shift, from reacting to understanding, is one of the most valuable upgrades any business owner can make.

Final Thoughts

Every business carries two kinds of costs, and every business owner benefits from knowing the difference. Fixed expenses set the floor. Variable expenses move with the work. One stays constant whether the month is busy or slow. The other rises and falls alongside every sale, every project, and every customer served. Recognizing which category each cost belongs to is not about becoming an accountant. It is about gaining the clarity to price with purpose, plan with confidence, and respond to change without guessing.

The business owners who struggle most with cash flow and pricing are often the ones who treat all expenses as a single number. They see the total at the end of the month and react to it rather than understanding what drove it. Separating fixed from variable expenses breaks that cycle. It breaks a confusing total into two clear categories, each with its own behavior and strategy. That separation is the foundation for every sound financial decision a business can make.

Watch It Instead

The Money Nudge — YouTube Channel

Prefer watching over reading? Every topic on this blog also comes to life as an animated video on our YouTube channel — where we make money talk even more simply.

Visit Our Channel