Illustrative Disclaimer: Any names, characters, or personal scenarios mentioned in this article are entirely fictional and created solely for educational purposes. They do not represent real individuals, events, or situations. Any resemblance to actual persons, living or deceased, is purely coincidental.

Two people work at the same company. They hold the same job title, earn the same salary, and take home the same paycheck every two weeks. From the outside, their financial lives look identical. Yet one of them is quietly building real security while the other slowly sinks. The salary does not reveal the difference. The car parked in the driveway does not reveal it either. Only one number tells the truth about where each person actually stands, and that number is net worth.

Most people measure their financial life by the size of their paycheck. Income feels like the scoreboard. It is the number we share, compare, and chase. Income is only half the story, though. It tells you how much money flows in, but it says nothing about how much you keep, what you owe, or what you have built over the years. Net worth fills that gap. It is the single figure that shows whether you are moving forward or falling behind, no matter your salary.

This article explains net worth in plain language. You will learn what it measures, how to calculate your net worth, and why it matters far more than the number on your pay stub. You do not need an accounting background to follow along.

Prefer to watch instead of read?

Subscribe to The Money Nudge on YouTube for plain-English videos on money, investing, and economic topics.

Table of Contents

What Net Worth Is and What It Actually Measures

Freeze your finances at one single moment, and you arrive at your net worth. The calculation lines up everything you own against everything you owe, then hands you one honest number. That figure can be large or small. It can even fall below zero. Whatever the result, it reflects reality more accurately than any paycheck ever could.

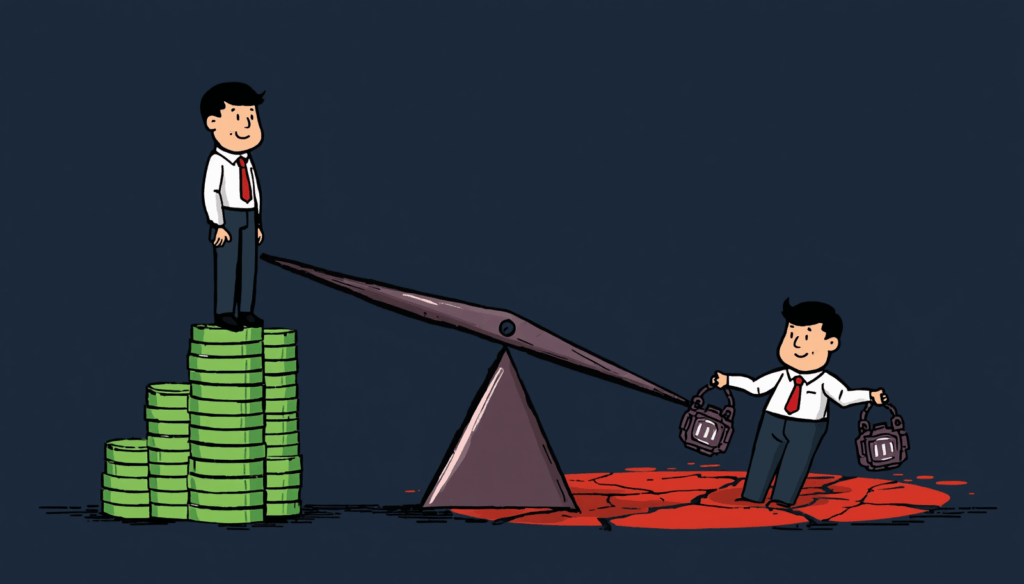

People often ask what net worth is, and the simplest answer is this. The number measures the gap between what you have and what you still owe. A paycheck shows the flow of money into your life. This figure shows what remains after the bills, the loans, and the spending settle out. Two workers can earn the same income for a decade and still end up in completely different places, because income measures speed, while the net worth number measures the distance you have actually traveled.

Picture income as the water pouring into a bucket. Your standing is the amount of water actually sitting in the bucket right now. A wide stream pouring in means very little if the bucket has holes in the bottom. Some people earn a modest income and keep almost all of it. Others earn a fortune and let it drain away through debt and spending. The pouring water gets all the attention, yet the level in the bucket determines whether you have something to draw on when life demands it.

This is why net worth, explained correctly, changes the way people see money. It shifts the focus from how much you make to how much you keep. That shift forms the foundation of measuring financial health in a way that actually means something.

Simple Steps To Break The Paycheck To Paycheck Trap

Read Article →The Net Worth Formula: What You Own Minus What You Owe

The net worth formula is refreshingly simple. You do not need a spreadsheet full of complicated math or a degree in finance to use it. The whole concept fits into one short line.

Net Worth = What You Own − What You Owe

In financial language, we call the things you own assets, and we call the things you owe liabilities. So you can also write the formula this way.

Total Assets − Total Liabilities = Your Number

That is the entire equation. You add up the value of everything you own, you add up the total of every debt you carry, and you subtract the second figure from the first. The result is your net worth. If your assets exceed your debts, the number is above zero. If your debts are larger than your assets, it falls below.

The beauty of this formula is that it does not care about your job title or your image. It does not reward the person with the nicest car or the biggest house. It only measures the truth. You will use this formula with far more confidence once both sides come into focus, so spend a moment on assets and liabilities and look closely at what counts as each.

The Compound Interest Can Be The Reason You Are Not Being Able To Build a Net Worth.

Read Article →What Counts as an Asset

An asset is anything you own that holds real, measurable value. If you could sell it for cash, or if it puts money into your pocket, it belongs on the asset side of your ledger.

Common assets include the money sitting in your checking and savings accounts. They include retirement accounts such as 401(k)s and individual retirement accounts. They include investments like stocks, bonds, and index funds. They include the current market value of your home if you own one, along with any other real estate you hold. A paid-off car counts, though its value drops each year. Even valuable personal items, such as jewelry, collectibles, or equipment, can count if they have meaningful resale value.

Here is a relatable way to picture it. Imagine you sold everything you owned today and gathered all the cash in one place. That total pile of money represents your assets. The house, the car, the savings, the retirement fund, the investments, all of it converts into a single number that shows what you have built.

One important point keeps people honest here. An asset is worth what someone will actually pay for it today, not what you paid for it years ago. A car you bought for thirty thousand dollars might sell for twelve thousand now. A phone you bought last year might fetch a fraction of its original price. When you list your assets, use the value they hold today, not the sticker price you remember.

Understanding What Is The Stock Market Will Help You Build Your Net Worth

Read Article →What Counts as a Liability

A liability is anything you owe to someone else. It is money that must leave your hands at some point in the future. Every debt you carry sits on this side of the equation, and it pulls your number down until you pay it off.

Common liabilities include your mortgage, which is usually the largest debt most people carry. They include car loans, student loans, and personal loans. They include credit card balances, medical bills, and any money you have borrowed from family or friends. If a person, a bank, or a company expects you to pay them back, that obligation is a liability.

A simple way to understand liabilities is to imagine every lender knocking on your door at once and demanding their money. The total amount you would owe across all of them is your liability number. It does not matter that you spread the payments across many years. The full balance still represents a claim on your future income.

This is exactly why two people with the same salary can live in two different financial worlds. One person keeps liabilities low and steadily turns income into assets. The other lets liabilities pile up and watches them quietly eat away at everything earned. The salary looks identical on paper, yet the bucket fills for one and drains for the other.

The Interest Rates Play a Crucial Role In Your Debt.

Find Out Why.

Read Article →Working Out Your Net Worth in Five Simple Steps

Knowing how to calculate net worth turns an abstract idea into a number you can actually use. The process takes about thirty minutes the first time, and it gets faster every time after that. Here is a clear, step-by-step method anyone can follow.

Step 1: List everything you own. Write down every asset you can think of and its current value. Include cash, checking, and savings balances, retirement accounts, investment accounts, the market value of your home, vehicles, and any valuable possessions. Be honest, and use the value each item holds today rather than the price you originally paid.

Step 2: Add up your assets. Total every number from the first step. This single figure represents everything you own. Try not to inflate it. An accurate number serves you far better than a flattering one.

Step 3: List everything you owe. Write down every debt and its current balance. Include your mortgage, car loans, student loans, credit card balances, medical debt, and any personal loans. Use the amount you still owe today, not the original loan amount.

Step 4: Add up your liabilities. Total every debt from the previous step. This figure represents the full claim other people have on your money.

Step 5: Find the difference. Place your asset total beside your liability total and subtract the debts from the holdings. The figure that remains is your net worth. That single result is the whole calculation, and you now hold a clear picture of where you stand.

The first time you run this calculation, the result may surprise you. Some people discover they own far more than they realized. Others find that their debts cancel out most of what they thought they had. Either way, you finally have an honest starting point, and an honest starting point beats a comfortable guess every time.

Do You Know What Tax Bracket Are You In?

Read Article →Why a High Income Does Not Always Mean a High Net Worth

A large salary feels like proof of financial success, yet income and what you keep are not the same thing. A person can earn an impressive paycheck and still hold a low or even negative net worth. This happens far more often than most people imagine, and it explains why the two coworkers from the opening story end up in such different places.

The reason comes down to a simple truth. Income measures how much money arrives. The figure we are discussing measures how much money stays. A person who earns $200,000 a year but spends every dollar on a large mortgage, two financed cars, frequent travel, and constant upgrades may end up with almost nothing. Meanwhile, a person who earns $60,000 a year and lives below their means can build assets steadily and avoid heavy debt. Over time, the modest earner can pull ahead of the high earner.

High earners often fall into a trap known as lifestyle inflation. Every time their income rises, their spending rises right along with it. A raise becomes a nicer apartment. A bonus becomes a new car. The paycheck grows, yet the bucket never fills, because the extra water flows straight out through new expenses. This is also how many people stay trapped in a paycheck to paycheck cycle even while earning what looks like a comfortable salary.

The lesson is clear. A high income gives you a powerful tool, but the tool only builds wealth if you actually use it to grow assets and reduce debt. Without that effort, a high salary simply funds a high-spending lifestyle while the number that matters stays flat or sinks.

Simple Steps To Break The Paycheck To Paycheck Trap

Read Article →Why Net Worth, Not Salary, Measures Real Financial Progress

Salary tells you how the world values your work this year. Net worth tells you how well you have managed everything you have earned across your entire life. One is a yearly headline. The other is the full story. When it comes to measuring financial health, the lifetime measure wins every time.

Consider how easily a salary can mislead. A person can land a high-paying job and feel wealthy overnight, even while carrying crushing debt and owning almost nothing. Another person can take a modest salary, save consistently, avoid unnecessary loans, and quietly build a strong position over the years. The first person looks richer at a dinner party. The second person actually is richer where it counts. The honest number cuts through the appearances and reports what is real.

Salary also disappears the moment you stop working. The wealth you have built does not. The assets you accumulate keep their value whether you clock in tomorrow or not. This is why the lifetime figure becomes the true measure of progress, especially as people think ahead to retirement. A paycheck supports you only as long as the job lasts. The wealth you accumulate supports you long after the paychecks stop arriving.

Tracking this figure instead of salary also changes your daily decisions. When you focus on it, you naturally ask better questions. You stop asking only how much you earn and start asking how much you keep. You begin to see spending, saving, and borrowing as moves that either raise or lower your real position. That shift, repeated over the years, separates people who build wealth from people who simply earn and spend it.

What a Negative Net Worth Means and Why It Is So Common

A negative net worth happens when your debts add up to more than your assets. In plain terms, you owe more than you own. The result looks alarming the first time people see it, yet it shows up far more often than most people realize, and it does not mean you have failed.

A large share of people carry a negative balance, especially early in adulthood. A recent graduate might leave school with $40,000 in student loan debt, a financed car, and very little saved. On paper, that person owes more than they own. This is not a sign of poor character or bad choices. It is the natural starting point for millions of people who borrowed to invest in their education or their independence before they had time to build assets.

The important idea is direction, not the single number. A negative figure that improves month after month is a healthy story unfolding in slow motion. Each loan payment shrinks your liabilities. Each dollar saved grows your assets. The gap closes a little at a time. Many people cross from negative to positive in their late twenties or thirties simply by paying down debt and saving steadily, without ever earning a dramatic salary.

So a negative number on your first calculation is not a reason for shame. It is a reason for clarity. It shows you exactly where you stand and provides a baseline for improvement. The goal is not to panic about today. The goal is to improve the number tomorrow, and then again the month after that.

How Your Financial Position Shifts Across Different Life Stages

Your financial position is not a fixed number that you reach and keep forever. It rises and falls across the seasons of life, and it follows a fairly predictable pattern for most people. Understanding this pattern removes a lot of anxiety, because it shows that a low number early on is normal rather than permanent.

In the early years, often the twenties, many people sit at or below zero. Student loans, low starting salaries, and the cost of setting up an independent life all weigh on the asset side. This stage is about building habits and chipping away at debt rather than reaching a big number. Slow progress here still counts as progress.

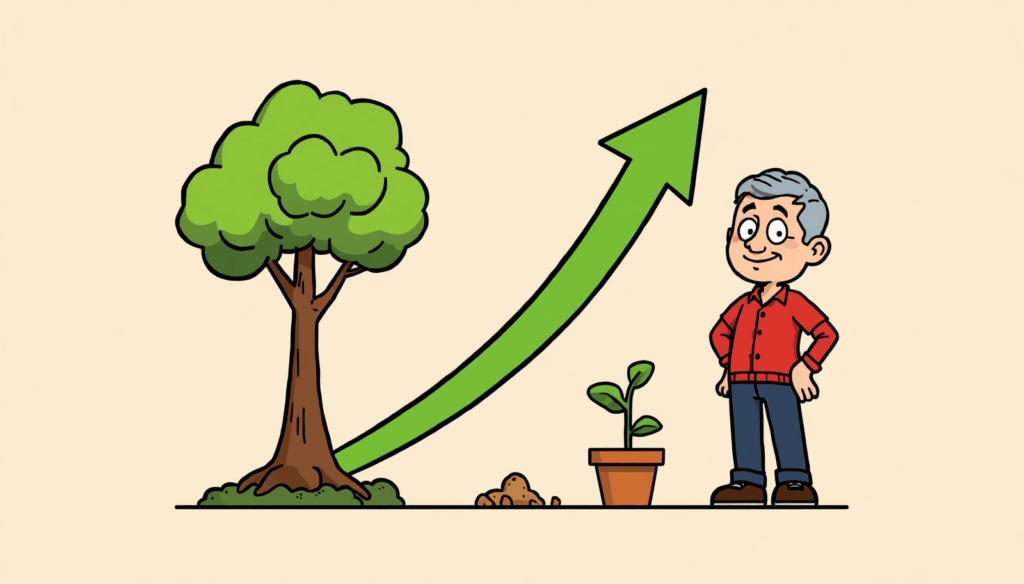

Through the thirties and forties, the picture usually begins to brighten. Incomes tend to rise, debts such as student loans shrink, and assets, such as retirement accounts and home equity, start to grow. This is often the stage at which consistent saving and the quiet power of compound interest begin to yield real results. Small contributions made years earlier start to multiply, and the gap between assets and liabilities widens in a satisfying way.

In the fifties and sixties, many people reach their peak. They finish paying down their mortgages, their retirement accounts mature, and decades of saving finally add up to a substantial figure. After retirement, the number often levels off or slowly declines as people draw on their savings to cover living expenses. That decline is normal and healthy because the whole point of building wealth is to support life when the paychecks stop. The key takeaway is patience, since each life stage carries its own normal range.

Why Tracking the Trend Over Time Matters More Than the Number Itself

A single figure tells you where you stand today. The trend over time tells you where you are headed, and the trend matters far more than any one snapshot. A person with a modest number that grows every quarter sits in a stronger position than a person with a larger number that shrinks each year.

Tracking your progress on a regular schedule turns vague feelings about money into clear evidence. Many people run the calculation once a quarter or once a year. When you do this consistently, you create a timeline of your financial life. You can see the months when you made real progress and the months when spending pulled you backward. That feedback is honest, motivating, and impossible to argue with.

The trend also protects you from short-term noise. Markets rise and fall. A rough month can dent your figure. A surprise expense can set you back. None of that matters much when you zoom out and watch the overall line climb across several years. One bad data point inside a rising trend is nothing to fear. A pretty figure inside a falling trend, on the other hand, deserves your full attention.

There is one more benefit to watching the trend. It rewards the right behavior. When you watch your progress climb because you paid off a loan or added to your savings, you connect your daily choices to a visible result. That connection builds momentum, and momentum is what carries people through the years it takes to build real wealth.

How Small, Consistent Decisions Compound Over the Years

Big numbers rarely come from one dramatic move. They come from hundreds of small, ordinary decisions repeated over many years. This is the most encouraging truth in all of personal finance, because it means you do not need a windfall to build wealth. You need consistency.

Picture two choices that seem minor in the moment. The first person sets aside a small amount from each paycheck and leaves it untouched. The second person spends that same amount on upgrades and impulse purchases. In a single month, the difference is barely noticeable. Stretch that same pattern across ten or twenty years, though, and the gap becomes enormous. The saver builds a growing pile of assets while the spender has only memories of the things bought.

Two forces make this happen. The first is the simple act of converting income into assets instead of expenses. Every dollar you keep and put to work moves to the strong side of the ledger. The second force is the way growth builds on itself, the same principle behind compound interest, where earlier gains start producing gains of their own. Money that stays invested or saved tends to grow, and that growth keeps growing. The earlier you start, the more time this effect has to work in your favor.

The practical message is freeing. You do not have to be perfect, nor do you have to earn a fortune. You only have to make slightly better choices more often than not, and then give those choices time to add up. Wealth rewards patience and consistency more than it rewards income or luck. A steady habit, repeated quietly for years, beats a single grand gesture almost every time.

Final Thoughts: The Number That Tells the Truth

The two coworkers from the beginning earned the exact same salary, yet they lived in two different financial realities. The paycheck hid that difference. Net worth exposed it. One person turned income into assets and kept debt low. The other let spending and borrowing drain everything away. Same salary, opposite outcomes, and only one number revealed which was which.

This single figure matters because it tells the truth that income cannot. It strips away the appearances and shows what you have actually built. It works the same way for a new graduate with a negative balance as it does for a retiree with a paid-off home. It does not care about your job title, your car, or the size of your last paycheck. It only reports where you stand and which direction you are moving.

If you have never run the calculation, the idea may feel intimidating, but the math is simple, and the payoff is real. Add up what you own, subtract what you owe, and write down the number. It does not have to be impressive. It only has to be honest. That single figure becomes your baseline, your starting line, and your scoreboard for the years ahead.

From there, the work is steady rather than dramatic. Keep your liabilities in check. Turn income into assets. Track the trend instead of obsessing over any single snapshot. Let small, consistent decisions add up over time. Do that, and the number will take care of itself. Income may be the headline, but net worth is the real story, and now you know how to read it. What Is Net Worth and Why Is It the Only Number That Truly Measures Your Financial Health may be the headline, but net worth is the real story, and now you know how to read it.

Watch It Instead

The Money Nudge — YouTube Channel

Prefer watching over reading? Every topic on this blog also comes to life as an animated video on our YouTube channel — where we make money talk even more simply.

Visit Our Channel